Outlook: The calendar today has retail sales, the usual jobless claims, two regional Fed surveys (NY and Philly), plus industrial production and business inventories. Analysts will parse the jobless claims but the real winner will be retail sales. So far the consumer is spending nearly as usual, if not a little more. At what point does that show a retreat? Again, if Chinese factory output (and port and shipping capability) falters, the American consumer faces shortages and higher prices next year–but will that inspire restraint? The cat laughed.

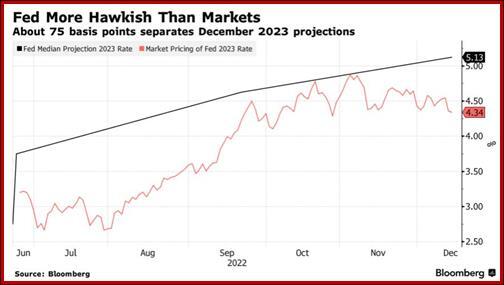

The dollar got sold off again on the Fed story, evidence that once again the markets and the Fed are not marching to the same drummer. The Fed said higher for longer and the CME FedWatcher tool showed a drop in the expected rates for next year, especially May, which shed 10 points. The yield curve steepened even as the Fed was forecasting positive growth all next year–only 0.5%, less than before, but not a recession. And yet all the big cheeses at the big banks foresee recession.

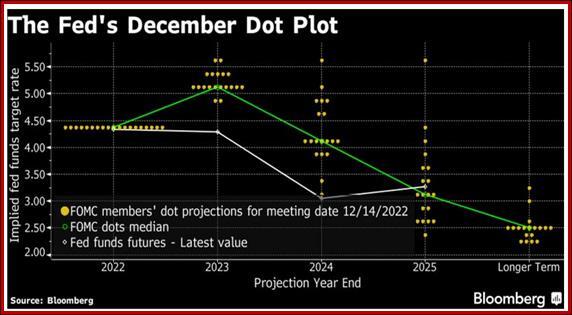

The message was very clear the battle has not been won, even if hiking is decelerating. Everyone expects two more hikes next year of 25-50 bp each to an ending rate of 5.1%. You’d think that would inspire some dollar buying, but as of the close yesterday, the charts didn’t back up that theory. A Bloomberg survey says 56% see a stronger dollar and a lower S&P. Since the 112 persons surveyed are named “investors,” they presumably have a stock market orientation.

A hefty 44% say they were surprised by how adamant the Powell sounded about not being done–“We still have some ways to go.” Mostly they were shocked by the new ending rate at 5.1% not expected to go down to 4.1% until 2024. As always, Powell said the Feb policy meeting will be data-dependent. As for that fictitious pivot we have been scornful about, ““I wouldn’t see us considering rate cuts until the committee is confident that inflation is moving down to 2% in a sustained way. Restoring price stability will likely require maintaining a restrictive policy stance for some time.”

In case you missed it, Powell also said “It is our judgment today that we are not at a sufficiently restrictive policy stance yet. We will stay the course until the job is done.”

The Fed believes that taming inflation absolutely, positively needs unemployment to rise in order for wage increases to moderate. No slack in the labor market, no wage relief. That means the unemployment rate next year has to go to 4.6% from 3.7% in November. We have doubts. The labor shortage is real and rising wages are not, so far, fixing it.

We have doubts about the Fed’s inflation forecast for next year, too–3.1% and falling to 2.5% in 2024, the earliest they can start, maybe, cutting rates. That is overly optimistic and assumes energy prices in the US remain tame, the war in Ukraine doesn’t make conditions any worse, the consumer gets the message to exercise spending restraint (ha), the government doesn’t overspend, price gougers relent, all supply chain issues magically vanish, and China doesn’t shut down again because of Covid.

Note that food and housing are the tow biggest components of rising inflation. Food still has rising prices. House prices may be stabilizing and even falling, which could give a false sense of improvement. And as always, the price of oil looms over everything.

If all the ducks line up to show inflation falling some more, we will get another dose of the market’s view that halting hikes and starting cuts will come sooner than Powell is saying. They seems to think inflation will come down faster and to lower levels than the Fed, and they are sticking to the 2023 pivot idea with sticky hands.

Nobody much is comparing rates in the various places, especially the ending rates. The US has a terminal rate expectation of 5.1%. The UK is at 3.5%, with 1% more expected, so a terminal rate of 4.5%. The ECB, assuming it does 50 bp today, has another 75 bp to go, ending with 2.75% next year. To be fair, the ECB is doing more TE per month than the US, and that has the same effect as some amount of tightening. The US expects a soft landing–no recession, if by the skin of our teeth, but both the UK and Europe are expected to enter recession, if they haven’t already.

Given this picture, why is the dollar soft? It doesn’t make sense. Opinion about the dollar’s futures is divided. Some say logic is always good, let’s go with a stronger dollar. Others say the soft landing is a fiction, let’s assume a weaker dollar that had been overbought in the first place and needs to fall some more to help the trade balance. We like logic but keep getting disappointed by outcomes. Apparently the anti-dollar sentiment is well-entrenched.

Tidbit: From Politico, news that the UN voted to remove Iran from a panel that promotes women’s rights. The resolution passed with 29 votes in favor of ousting Iran and eight votes against. Sixteen countries abstained. The proposal came from the US (at last) after the murder in September of a women wearing too little headscarf by Iran’s “morality police.” Iran never belonged on the Commission on the Status of Women in the first place.

Tidbit: The stories about the arrest, extradition and indictment of the crypto guy SBF are entertaining. The Bahamas wants to prosecute him in their country, but the US wants him home, saying they do not trust the Bahamians. SBF, having shown up in shorts and t-shirts for big events with the likes of formers PM Blair and Pres Clinton, wore a jacket to get arrested. Bloomberg reports “The grim conditions FTX founder Sam Bankman-Fried is encountering in the Bahamas prison where he’s currently being held could change his attitude on extradition to face fraud charges in the US.” As the first guy in the crypto world to get caught with so much evidence left behind, including keeping records with Quickbooks, we bet they throw away the key.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

previous

previous