S&P 500 didn‘t break the3,905-3,910 zone, not even overnight. Most tellingly, USD couldn‘t catch a proper bid on yields turning sharply up, and commodities in the black merely confirm risk-on sentiment to win today. The bears fumbled during the European sessions, and the relative performance of value and tech highlights where to look for gains today (in the cyclicals).

See the turn in intraday appreciation for oil (always good when the laggard wakes up – silver with copper continue to lead gold, and miners are to do very well) as it relates to the dollar, and how USD‘s intraday reversal reflects on what‘s to come today – already today, and not after tomorrow‘s PPI release:

(…) The key catalyst to look for in terms of upside fuel, is Friday‘s PPI that‘s likely to show slowdown in inflation, and then Tuesday‘s CPI probably to come at 7.5 or 7.6% YoY, which would once again (in both cases) feed into the „Fed would now really go slow on tightening aka pivot“ angle that markets are way too willing to run with. Willing as in misguided, because the Fed isn‘t getting less restrictive at all – see rate hiking and balance sheet shrinking combined, effects to play out still. No better indicator of demand destruction to come than the price of oil really – sign of caution.

Referring to the title, it‘s the USD-yields-commodities interplay, which will result in nice day of real asset trailed by stocks market gains.

Keep enjoying the lively Twitter feed serving you all already in, which comes on top of getting the key daily analytics right into your mailbox. Plenty gets addressed there, but the analyses (whether short or long format, depending on market action) over email are the bedrock. So, make sure you‘re signed up for the free newsletter and that you have my Twitter profile open with notifications on so as not to miss a thing, and to benefit from extra intraday calls.

Let‘s move right into the charts.

S&P 500 and Nasdaq outlook

No break of the 3,905 – 3,910 support, declining volume, and crucially the above mentioned inconsistencies within the bearish push as 3,910 didn‘t break overnight regardless of a good run at it aftermarket when the bears still had the initiative that was lost during the European session only. 3,965 followed by 3,980 are the upside levels.

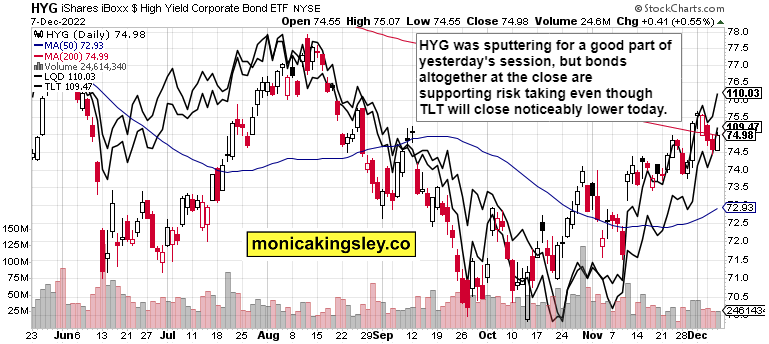

Credit markets

HYG recovered from intraday weakness into the close, and that was constructive – even if junk bonds underperformed TLT. During the European morning, the market shook this off, and will continue to add to gains.

previous

previous