Outlook: This week is a short one in the US because Thanksgiving comes on Thursday and while markets are open on Friday, lots of folks make it a 4-day weekend–trading will be thin in every class. Somewhat strangely, the news of the week may well be the minutes of the last FOMC meeting on Wednesday, since we are all trying to read the Fed’s mind. We guess the minutes will show a relentlessly hawkish tone. You have to wonder if the markets will “get it” at last.

We also get the S&P flash manufacturing and services PMI’s, durables, the Riksbank, the Reserve Bank of New Zealand, and the minutes of the last ECB policy meeting. The S&P composite PMI is forecast down a hair to 48.0 from 48.2 in Oct, led by manufacturing (50.0 from 50.4) with services at 48.0 from 47.8. We also get a slew of regional Fed reports, starting with the Chicago national today, expected down to -0.03 from 0.10 in September. Remember that in this measure, zero means “on trend,” so despite being the first negative reading since June, it’s not actually “bad” but rather a sign of ongoing resilience.

About the Fed: The bond gang got it, a little. The expectations-sensitive 2-year rose to a one-week high on Friday and closed at 4.514% after spending most of the week under 4.4%. That seems a feeble response to Bullard’s over 5% and maybe as much as 7% for Fed funds. And check out the 10-year—not out of the woods.

The CME FedWatch tool—so badly designed and presented in tiny fonts—shows that those expecting 5.25-5.5% by June next year rose from 8.3% last week to 22.5% in the latest reading, up in one day from 19.4%—but it was 16.4% the month before. Those seeing 5.50-7.75% rose to 4.8% from zero and those seeing 5.75-6.0% rose only to 0.3% from zero.

We may get some leadership from the Reserve Bank of New Zealand, which meets on Wednesday and forecast to hike another 75 bp (to 4.25%), but maybe only 50 bp, which is what it did at the Oct 5 meeting. Inflation is at 7.2% y/y in Q3.

We will not publish any reports on Thursday or Friday. That means we will miss Germany’s IFO and GfK plus a slew of other releases.

As the week gets going, we see three drivers—the Fed minutes, the Reserve Bank of NZ, notable for sanity and reasonableness, plus realistic forecasts—and China’s Covid policies. Bloomberg reports risk aversion arising from Covid setbacks in China is the driver of the dollar today. It’s also presumably the driver for the AUD—to the downside.

It’s an easy jump from China crackdown to supply shortages and supply chain problems. Remember that earlier this year, China closed ports as well as factories, inhibiting imports as well as exports. If we get a repeat, that means inflation in the US and Europe gets a punch in the nose, again. Does this influence the economists beavering away in the back rooms of the Fed, BoE and ECB? We bet they are keeping an eagle eye on it.

We also guess that renewed crackdowns in China, if that’s what we get, raise the probability of recession pretty much everywhere. Assuming inflation remains the top priority, it doesn’t tell us anything about what central banks will do, but tickles the odds to more hawkishness.

Recession Tidbit: The WSJ reports the pile of savings built up during the pandemic is already shrinking and will be used by in 9-12 months. Those stimulus checks plus “constrained spending opportunities” resulted in excess savings of $1.2-1.8 trillion.

“As those savings dwindle, signs of financial stress could reappear, such as rising default rates on loans. That stress could get more pronounced if the labor market slows. Economists surveyed by The Wall Street Journal expect employers will start cutting jobs in the second and third quarters of next year.”

This report comes from an Oct report by the Fed that helpfully defines how savings can be “excessive” and what they look like across income segments. It’s pretty interesting that the Fed conclusion is different (positive) from the WSJ’s (negative). “In summary, our estimates suggest that households across the income distribution continue to have a buffer of excess savings to help them navigate higher prices and/or a tightening cycle. While this buffer is dwindling, for now it is likely still providing some needed balance sheet support that could help to stanch a negative feedback loop were the economy to slow.”

US Politics: The Attorney General has appointed a special counsel, a puritanical-looking guy named Jack Smith, to take a leadership role now that Trump has generated “special circumstances” by running for office. The amount of commentary on this action, much of utterly false, is astounding. The important thing—the first 2024 presidential primary in New Hampshire is only a little more than a year away—and the country needs indictments and trials before then.

And child genius Musk is letting the Orange Menace back on Twitter. Gee, what can go wrong?

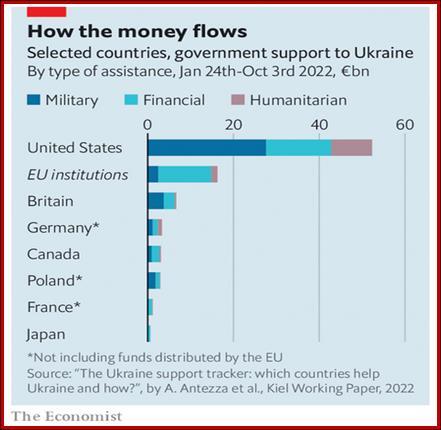

Foreign Affairs Tidbit: The Economist last week showed this little chart that contains a world of meanings. It would be nice to see the dollar amounts or maybe dollars per capita, but never mind—it’s clear that once again it’s the US defending Europe from itself.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

previous

previous