A flurry of central bank meetings in Central and Eastern Europe next week mark the last major events before the festive season gets underway.

Hungary: Central bank unlikely to deliver changes to 'whatever it takes' stance

The National Bank of Hungary (NBH) has made it clear on several occasions that the temporary and targeted measures, introduced in mid-October, will remain in place until there is a material and permanent improvement in the general risk sentiment. Although we’ve seen some progress here, we don't think enough has changed to trigger an adjustment in the monetary policy’s hawkish “whatever it takes” setup. See our preview here.

Regarding the current account balance, we expect a significant deterioration compared to the second quarter. We see the deficit widening on energy items, considering the country’s energy dependency combined with significantly higher prices paid in hard currency.

Czech Republic: Last CNB meeting of the year to confirm a dovish majority

The Czech National Bank (CNB) will hold its last meeting of the year on Wednesday. We expect it to be a non-event, with rates and FX regimes unchanged. The new forecast will not be released until February, so it is hard to look for anything interesting at this meeting. Board members have been very open in recent days and hence there is minimal room for any surprises. The traditional dovish majority has publicly declared that interest rates are high enough and continue to choose the “wait and see” path. As always, we have heard warnings that interest rates could go up if necessary. However, the near-zero market reaction shows that the dovish view here is clear. The governor also confirmed this week that the central bank will continue to defend the koruna. At the same time, another board member confirmed that the CNB has not been active in the market for some time. So hard to look for anything new here either.

Turkey: Central bank to keep policy rate unchanged

We expect the Central Bank of Turkey (CBT) to keep the policy rate unchanged at 9% in December, having confirmed last month that it had reached the end of the easing cycle by stating that the current level of the policy rate is adequate. However, there are continued expectations for some easing in the current banking sector regulations, along with targeted credit stimulus measures such as Credit Guarantee Fund (CGF) loans. Given the CBT’s signal of strengthening the macro-prudential framework, the release of the “2023 Monetary and Exchange Rate” document will also remain in focus.

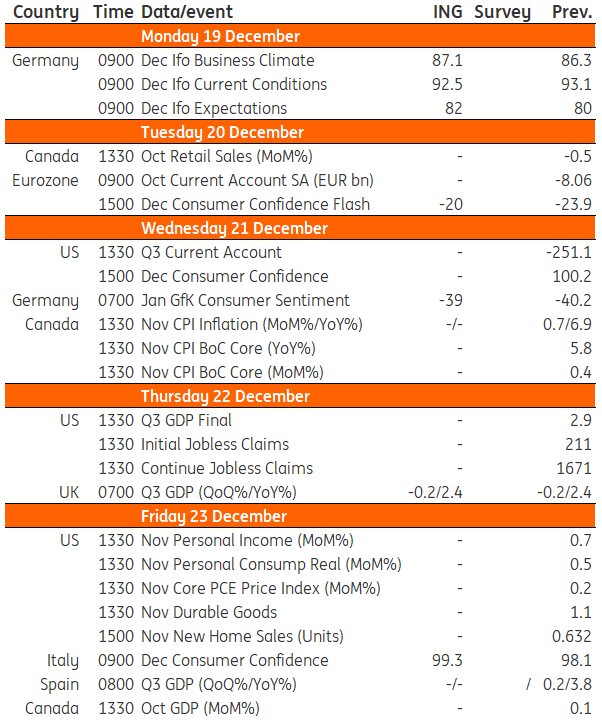

Key events in developed markets

Source: Refinitiv, ING

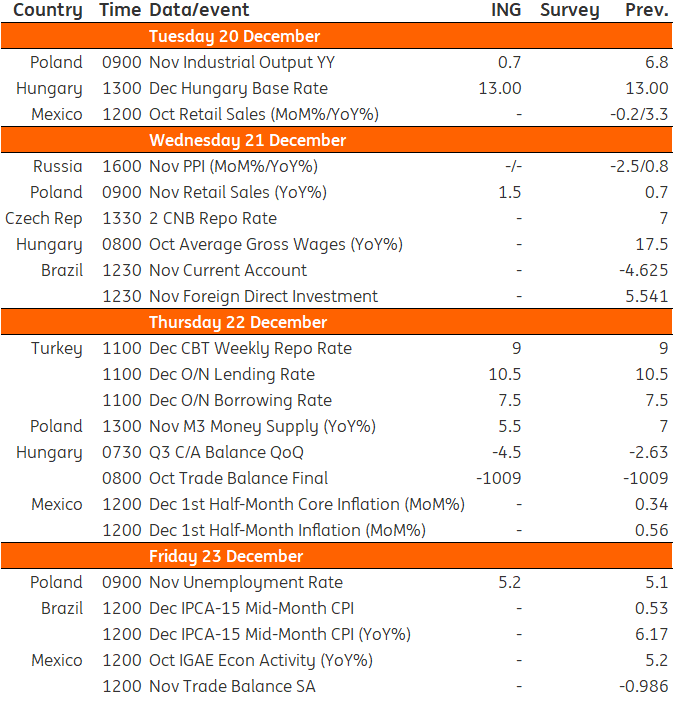

Key events in EMEA/LATAM next week

Source: Refinitiv, ING

Read the original analysis: Key events in developed markets and EMEA next week

previous

previous