S&P 500 did another daily reversal, but the bears haven‘t yet won. The risk-on in stocks hasn‘t been broken as value demonstrates, but bonds are getting the macro picture right, as they often do – the Fed is to remain hawkish as Daly reaffirmed, which would help keep real assets in check while that lasts. Precious metals proved their sensitivity to sharp increases in yields – this recognition of the tightening reality played out on the long end of the curve, not affecting the continued rate raising expectations for Sep FOMC really (regardless of the inconsistent market interpretations of both CPI and PPI).

S&P 500 and Nasdaq outlook

Even if S&P 500 pushes higher today on better-than-expected consumer sentiment data (relief at the pump), the bears are likely to break below the 4,212 support next week (if not later today already).

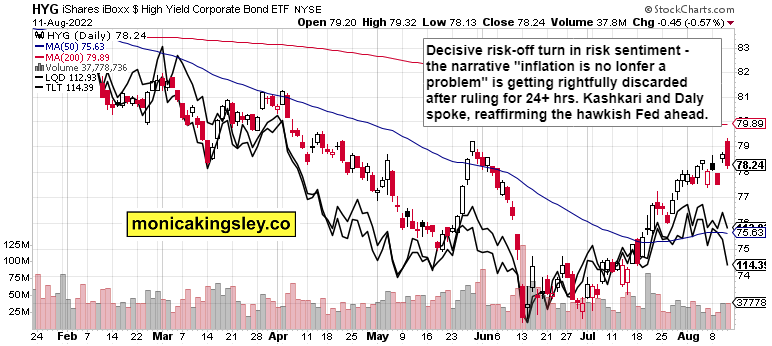

Credit markets

HYG is likely to retrace a part of yesterday‘s reversal – a proper reversal as the volume confirms while quality debt instruments would play a lesser role in moving stocks today. Clearly, bonds aren‘t bullish here, and the deterioration is to continue over the weeks ahead.

Bitcoin and Ethereum

Similarly in cryptos, no game-changer happened, and the rally is looking tired.

previous

previous