Summary

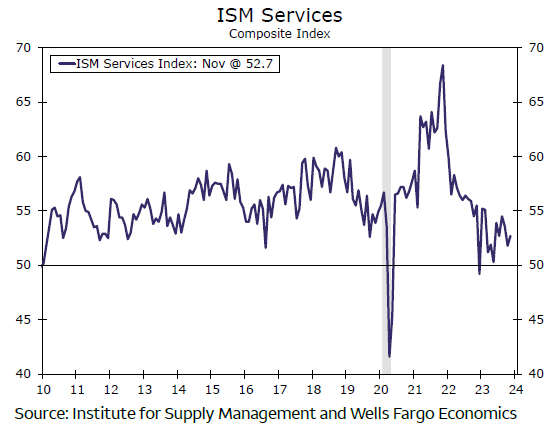

Not only is the services sector still expanding, it picked up steam in November with the ISM coming in at 52.7. With prices still firmly in expansion and employment rising slightly, it suggests that recent expectations for rate cuts might have been pulled too far forward.

Two years before the mast

It’s been quite a journey the past two years. In November 2021, the ISM services index reached its zenith, not just for this cycle, but in records dating back to the 1990s. The fed funds rate two years ago was still at the zero lower bound and inflation was still ascendant. In the ensuing 24 months, the Fed embarked on a rate-tightening campaign for the ages, yet despite a fed funds rate now higher than any point in more than 20 years, the Fed’s job is not quite finished. Yes, inflation is coming down, but is still above the Fed’s 2.0% target and the ISM services index is still in expansion territory, even if unconvincingly so at 52.7 (chart).

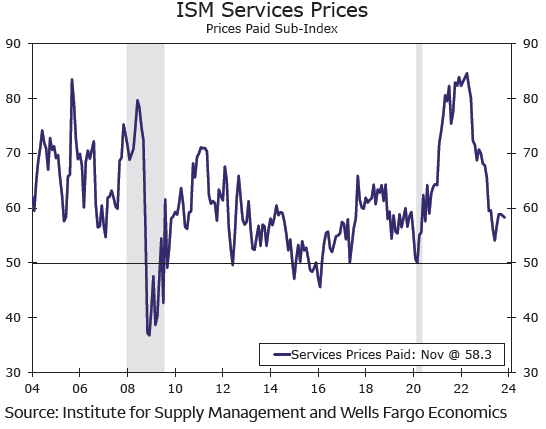

The trouble is that while the service economy may be able to withstand higher capital costs, big-ticket durable goods spending is more vulnerable to higher rates. But as long as services outlays remain robust, there is little incentive for service providers to lower prices. This complicates the Fed’s efforts to get inflation fully in check. To the extent that the service sector keeps humming along, it could dash the rising hope in financial markets that rate cuts are just beyond the horizon. It is tough to justify cutting rates when the prices paid component is still consistent with rising prices (chart).

Download The Full Economic Indicator

previous

previous